By Luisa Maria Jacinta C. Jocson, Reporter

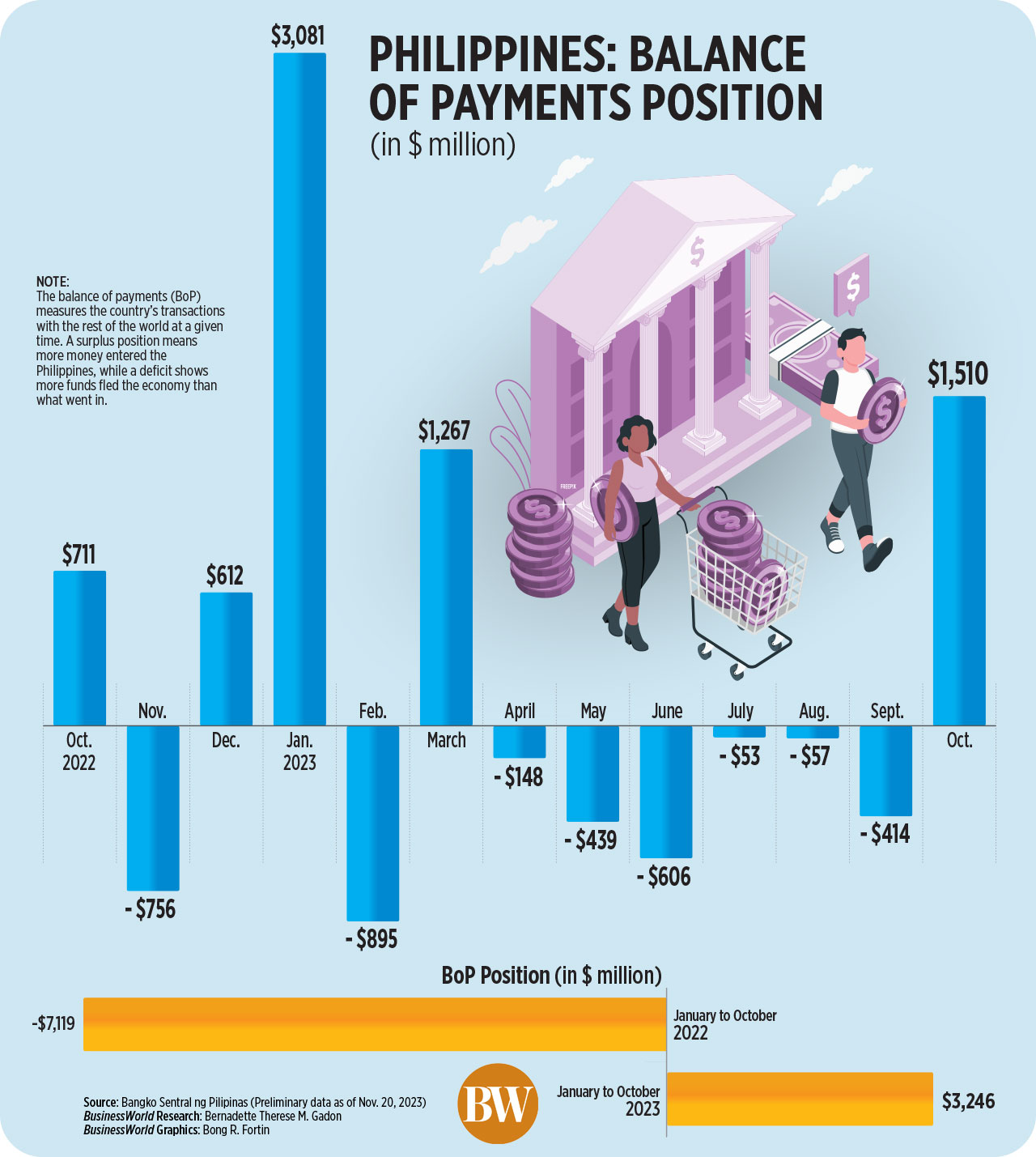

THE PHILIPPINES’ balance of payments (BoP) position swung to a surplus in October, ending six straight months of contraction, the central bank said.

Data released by the Bangko Sentral ng Pilipinas (BSP) showed the country’s BoP surplus widened to $1.5 billion in October from $711 million in the same month a year ago.

Month on month, this was a turnaround from the $414-million deficit in September.

{kind=link}

October also saw the biggest BoP surplus since the $3.081 billion recorded in January.

“The BoP surplus in October 2023 reflected inflows arising mainly from the National Government’s (NG) net foreign currency deposits with the BSP, and the BSP’s net foreign exchange operations and net income from its investments abroad,” the central bank said.

The BoP is a gauge to show the country’s economic transactions with the rest of the world at a given time. A surplus shows that more money flowed into the Philippines than what had exited, while a deficit means more funds fled the economy.

In the first 10 months of 2023, the BoP position stood at a $3.2-billion surplus, a turnaround from the $7.1-billion deficit in the same period a year ago.

“Based on preliminary data, this development reflected mainly the improvement in the balance of trade alongside the higher net inflows from personal remittances, trade in services, and foreign borrowings by the NG,” the BSP said.

Preliminary data from the local statistics agency showed that the trade gap narrowed by 14.7% to $39.82 billion in the January-to-September period from the $46.69-billion deficit a year ago.

In September alone, the trade deficit shrank by 27% year on year to $3.51 billion from the $4.83-billion gap recorded in the same month in 2022.

The BSP also said the net inflows from foreign direct investments also contributed to the BoP surplus.

China Banking Corp. Chief Economist Domini S. Velasquez said that the improving BoP position was due to lower merchandise trade deficits and bigger inflows through investments, remittances, and trade in services.

“Service exports have recently played a bigger role in the country’s balance of payments, compensating for some softening in merchandise trade,” she said in a Viber message.

At its end-October position, the BoP reflected a final gross international reserve (GIR) level of $101 billion, up by 2.96% from $98.1 billion as of end-September.

The dollar reserves were enough to cover 5.8 times the country’s short-term external debt based on original maturity and 3.7 times based on residual maturity.

It is also equivalent to 7.5 months’ worth of imports of goods and payments of services and primary income.

Rizal Commercial Banking Corp. Chief Economist Michael L. Ricafort said that the NG’s latest retail dollar bond offering also led to the higher BoP surplus and gross international reserves.

The Philippine government raised $1.26 billion from its first retail dollar bond offering under the Marcos administration, which was offered from late September to early October.

Ms. Velasquez expects the country’s BoP position to further improve in 2024, driven by a “general recovery of the global semiconductor industry, boosting Philippine merchandise exports.”

“For the coming months, BoP data could still improve with the continued increase in the country’s structural inflows as the economy reopens further towards greater normalcy,” Mr. Ricafort added.

The BSP expects the country’s BoP position to end the year at a $127-million deficit. Next year, the central bank sees the BoP position to end at $1-billion surplus, equivalent to 0.2% of GDP.