There are two good economic developments in the Philippines recently. Let’s go straight to the numbers.

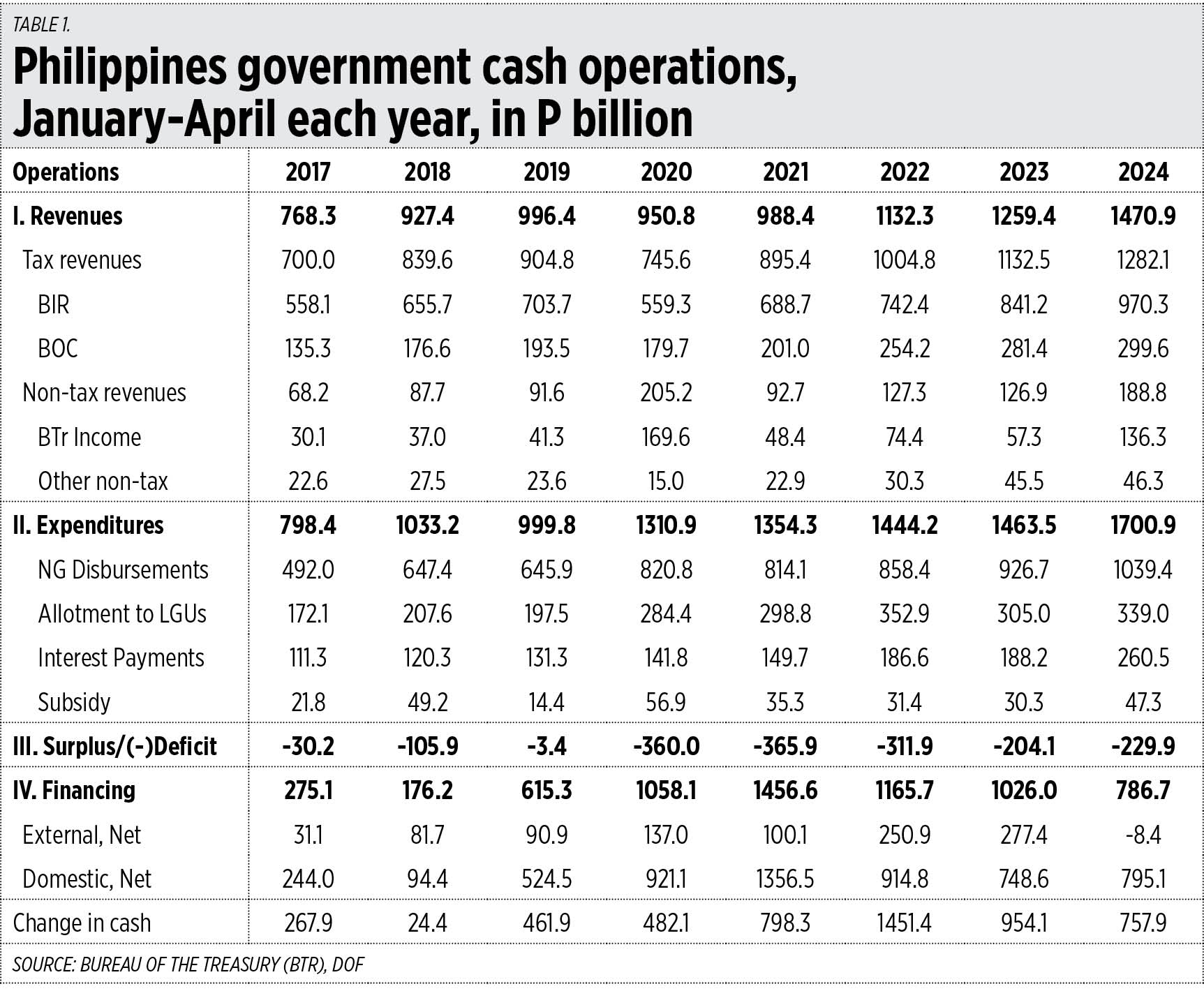

DECLINING DEFICIT AND BORROWINGSIn the first four months of 2024, revenues reached P1.47 trillion, 17% higher than P1.26 trillion a year earlier. This is significant for two reasons. One, a high percentage increase despite no tax hike this year, better tax administration and higher nontax revenues. And two, the 17% revenue increase is twice as high as the 8.8% increase in GDP at current prices in the first quarter from a year ago.

But expenditures in January to April 2024 reached P1.7 trillion, 16% higher than P1.46 trillion a year earlier. So the budget deficit was P230 billion, 12.7% higher than P204 billion a year ago but 26% lower than P312 billion in 2022 and 37% lower than P366 billion in 2021.

Financing or borrowings in January to April 2024 was only P0.79 trillion, the first time it fell below P1 trillion since 2020. There was a big drop in foreign or external financing — P8 billion in 2024 vs P277 billion in 2023, which is a good development (see Table 1).

{kind=link}

The jump in expenditure came from National Government (NG) disbursements and interest payment due to a high public debt stock and the high interest rate policy. Interest payment this year already reached P260 billion or twice the P131 billion in 2019. There is a need to significantly reduce the public debt level to save resources for social and infrastructure needs instead of diverting these to higher interest payments.

Related recent stories in BusinessWorld on the fiscal situation were “GOCC subsidies more than triple in April” (June 9), “LGUs to receive P1.034-trillion NTA in 2025” (June 16), “PHL gov’t should consider raising taxes, analysts say” (June 17).

In the last report where I was one of the quoted analysts, I argued that there is no need to raise taxes because there are short- to long-term sources of additional revenues. For instance, Finance Secretary Ralph G. Recto has raised the dividends that government-owned and -controlled corporations (GOCCs) should remit to NG to P100 billion in 2024 alone. Many of the GOCCs also raised their dividend payments to NG from a minimum 50% to 75%.

Better tax administration will also help control illicit trade and smuggling, especially of tobacco products. I elaborate on the privatization of several government land assets soon.

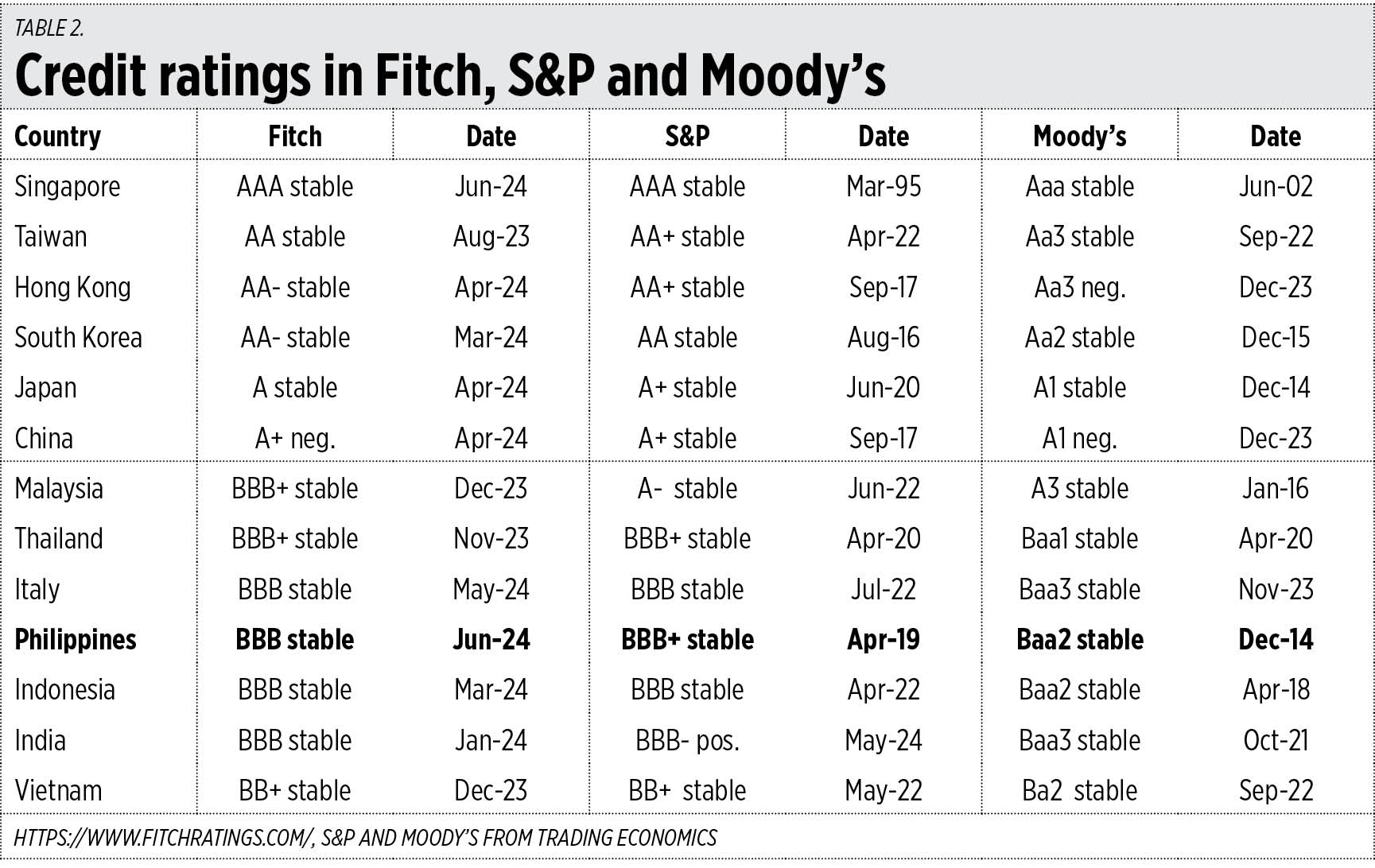

IMPROVING CREDIT RATINGSOn June 7, Fitch ratings released a report where it affirmed the Philippines at ‘BBB’, with a stable outlook. This is good news. I checked other Asian economies in Fitch Ratings, and I added two other prominent rating companies — S&P and Moody’s. The Philippines is near “A” ratings and we may be able to overtake Italy and Thailand and be at par with Malaysia soon (see Table 2).

{kind=link}

I particularly like this part in the Fitch report where they noted that “The Finance secretary has publicly indicated that no new taxes would be imposed in 2024, and possibly until the end of the Marcos Jr. administration in 2028. Nevertheless, we note that overall budget balances have tended to be close to the targets in recent history.”

There were three reports in BusinessWorld related to this — “Finance secretary wants to keep original revenue goals” (June 5), “Recto says Philippines still on track to achieve ‘A’ credit rating” (June 10) and “Banking industry outlook is ‘improving,’ says Fitch” (June 12).

Secretary Recto is correct in making an optimistic announcement that “this affirmation is highly encouraging as it shows a strong vote of confidence in our ability to grow the Philippine economy in a higher path over the medium term… We are on the road to an ‘A’ rating. A better credit rating will help us create more jobs and reduce poverty by 2028.”

Budget Secretary Amenah F. Pangandaman expressed the same optimism, saying that “It bears noting that Fitch cited the Philippines’ strong medium-term growth as one of the reasons for our rating. We hope to sustain our momentum for growth and keep our lead as one of the fastest-growing economies in Southeast Asia.”

On spot there, Mr. Recto and Madame Pangandaman. We just need to sustain high GDP growth of 6% or higher for several years while controlling borrowings so that the public debt/GDP ratio can be reduced and by extension, cut the budget deficit target of 3.7% of GDP by 2028. Productivity-enhancing budgetary spending like infrastructure should continue while wasteful spending like endless subsidies and freebies that lead to endless state dependence, war preparations and military and uniformed personnel pensions from the budget should be controlled.

In 2019, the debt-to-GDP ratio of the Philippines was only 37%, while Thailand had 41% and Malaysia had 57%. When the lockdown was imposed in 2020, their respective ratios jumped to 51.6%, 49.4% and 67.7%. By 2023, their respective ratios were 56.6%, 62.4% and 67.3%.

In average GDP growth from 2021-2023, the Philippines had 6.3%, Malaysia had 5.2% and Thailand had 2%. So in both reducing the debt-to-GDP ratio and raising overall growth, the Philippines had better performance than Thailand and Malaysia. From these two important metrics, the Philippines overtaking Thailand and being at par with Malaysia in credit ratings are a realistic and desirable trend.

Bienvenido S. Oplas, Jr. is the president of Bienvenido S. Oplas, Jr. Research Consultancy Services, and Minimal Government Thinkers. He is an international fellow of the Tholos Foundation.